Whether you’ve owned a home before, or you’re ready to jump into homeownership for the first time, there are always a lot of questions swirling around about what is truly required for a down payment, and how to best source down payment assistance. Let’s tackle these two today.

1. How much do you really need for a down payment?

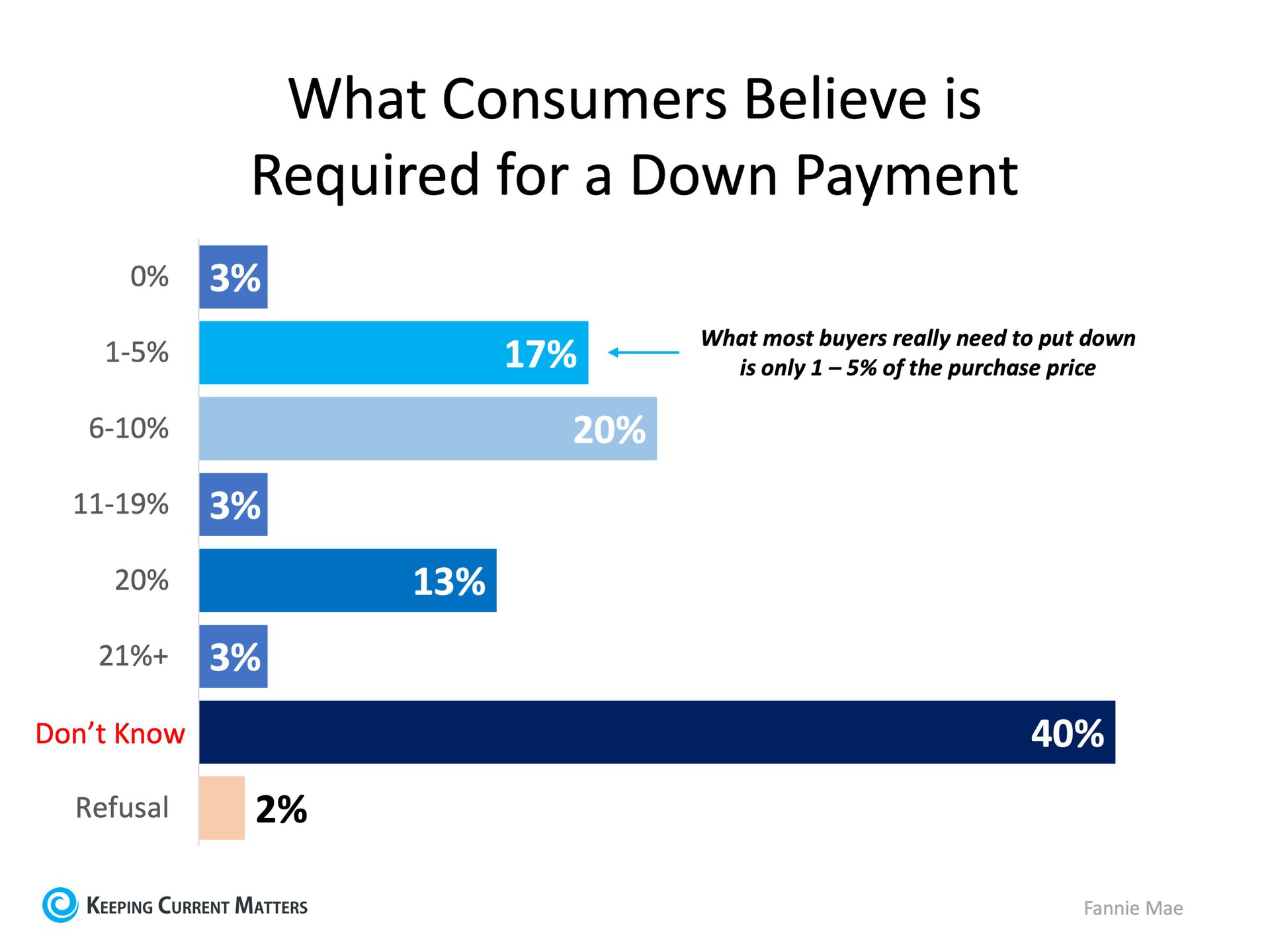

There is a long-standing misconception about down payment requirements. A survey from Fannie Maeshows only 17% of consumers know the minimum options are actually between 1 – 5% of the purchase price and 40% don’t know how much they need at all.There are many mortgage loans available that require as little as 3% down for first-time buyers, and some ask for only 3.5% down from repeat buyers. There are even loans available for Veterans that provide 0% down payment options too.

{kind=link}

We’ve mentioned recently that you don’t need to come up with a 20% down payment to buy, and we’ve also shared how quickly you can save for a 3% or 10% down payment, depending on where you live. If you’re planning to put down just 3%, the research shows it may be possible in most states to have enough saved for a down payment in less than a year. That puts homeownership in a much closer reach for many potential buyers, maybe even you!

2. How can I get help with my down payment?

Regardless of the loans available, many buyers still need assistance with a down payment. The great news is, there are a lot of ways to tap into down payment assistance options. Here are just a couple of them:

The Bank.

Okay, this is the obvious source. From a checking or a savings account, accessing readily available cash from a bank account is the most common. Consumers can save up a little each month until the minimum amount of funds needed have accrued. The lender will ask for copies of the most recent bank statements showing available funds as well as documenting the source of those funds. Most often the deposits are from an employer via direct deposit. Self-employed borrowers who do not receive a regular paycheck on the 1st and 15th will be asked to provide business bank statements as well.

A Gift.

The National Association of Realtors (NAR) said, “a third of recent first-time buyers received down payment assistance from family members.” They also mentioned, “the average net worth of those aged 75 and over stands at $264,800…They just might offer the boost the next generation needs to become homeowners.”

There are those fortunate few who do receive a financial gift from a family member. Gift funds must also be tracked to make sure the funds are coming from an acceptable source. Gift funds can come from a family member, relative, or someone in a committed relationship. Lenders want to make sure the gift funds aren’t a loan that must be paid back at some point in the future. There needs to be a signed “gift letter” included with the loan file stating the amount of the gift, the donor’s name and where the funds are coming from. Lenders won’t ask for bank statements from the donor, but do want to know the funds came from an account in the donor’s name.

A Retirement Account.

If someone has a retirement account with an employer such as a 401(k), that person can take out a loan against the fund. This is allowable per lending guidelines but is also subject to the employer’s approval. Most retirement funds allow for someone to borrow up to one-half of the employee’s vested balance in the account. With an IRA, first time buyers can withdraw up to $10,000 without penalty. The withdrawal will still be subject to any income tax due.

An Appraisable Asset.

If someone owns something that can be appraised by an independent third party, the proceeds when selling that asset are an acceptable source. Selling an automobile is acceptable, for instance because it has an appraised value. Even a highly prized baseball card is an appraisable asset. It’s important to document the transaction from the initial sale to the deposit in the account.

A Down Payment Assistance Program.

Down payment assistance programs are typically overseen and/or issued by a county or state agency. Such programs typically require the borrowers’ gross monthly income to not exceed certain limits and are often available to first time buyers. These programs can also be geographically targeted to help low to moderate income communities flourish. Down payment assistance can come in the form of a grant, which means there is no repayment required, or a loan which can be forgiven after living in the property for a certain period of time, typically three years or more.

There are, however, more than 2,500 down payment assistance programs available (by local areas like city, county, or neighborhood), and some of them are even specifically for first-time buyers.

The gap, as mentioned in the same survey, is “only 23% of consumers are familiar with low down payment programs.”

That’s why it is so important to get familiar with these options by doing your homework before you plan to buy a home. Determine what is available in the area where you ultimately want to live, so you have all the details you need to take advantage of the down payment assistance option that is best for your family.

Bottom Line

If buying a home is one of your long-term goals, you may be able to get there sooner than you think by tapping into one of the many down payment assistance programs available.

Leave a Reply